Personal Contract Purchase (PCP)

Explore how PCP finance makes driving a car more affordable

What is Personal Contract Purchase?

Personal Contract Purchase (PCP) is one of the most popular and flexible ways to finance a car, both new and used, offering a personalised solution tailored to your needs and lifestyle.

With PCP, you will drive a vehicle for an agreed period, typically 2 to 4 years, based on a mileage limit chosen at the start of your agreement. During this time, you make fixed monthly payments that cover the car's depreciation, not its full value.

The monthly cost is calculated by estimating the difference between the car's initial price and it Guaranteed Future Value (GFV) - the predicted value at the end of your agreement, assuming you stay within the mileage limit.

Another key advantage of PCP is that the GFV is locked in from the start, which protects you from market fluctuations, so you will know exactly what your car will be worth at the end of the term.

Browse our new car offers by selected your preferred car manufacturer.

What does a PCP Finance deal typically look like?

At a first glance, PCP agreements may seem rather complex, but actually they are one of the most straightforward and flexible ways to finance a new car. They offer a clear structure and multiple options at the end of the term, making them a popular choice for many drivers.

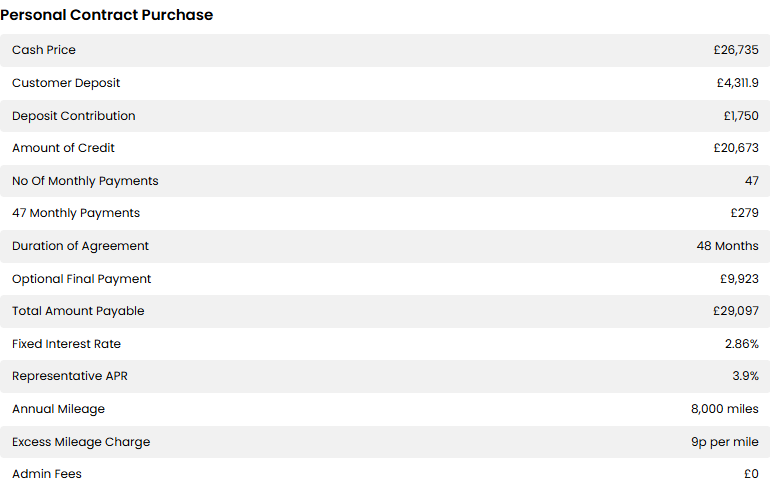

Here's a typical example of how a PCP finance deal is structured:

What the key terms mean:

Total Cash Price/On the Road Price: This is the price of the vehicle to purchase outright without finance or interest charges.

APR Representative: Annual Percentage Rate (APR). This is the rate of interest the lender charges, this will stay the same throughout your agreement.

Total Amount Payable: This is the total amount paid by a customer after fully completing a PCP contract. Including the deposit, monthly payments, guaranteed future value and any interest charges.

Optional Final Payment: This is the predicted value of the vehicle you have purchased once you reach the end of your contract. When the agreement is over, you will have the option to purchase the vehicle at this price, often referred to as a balloon payment.

Amount of Credit: This is the amount of borrowed finance you will receive to cover the cost of the vehicle at the start of the agreement. This is the price of the car, minus the deposit you have paid and any deposit contribution.

Customer Deposit: The upfront deposit paid by a customer at the start of an agreement.

Deposit Contribution: This can be found on new car finance deals and is a deposit contribution from the manufacturer as an incentive for customers.

Annual Mileage: This is the number of miles you can use the car for per year. This is agreed at the start of your agreement and is used to help predict the depreciation and vehicle value at the end of your agreement.

Excess Mileage Charge: The amount charged per mile if the annual mileage is exceeded.

Option to Purchase Fee: This is an additional fee that a customer may need to pay to gain ownership of their vehicle.

Why Choose Personal Contract Purchase for your next car?

A very popular choice for car finance, PCP offers a range of benefits:

New vehicles accessible

Option to make it yours at the end

Flexible agreements

GFV guaranteed at the start of your agreement

Frequently Asked Questions about PCP agreements

Do I own the car during the agreement?

What is GFV?

Can I settle my PCP agreement early?

What happens if the car is worth more than the GFV?

What happens if I damage the car?

Please provide your details below and a member of our team will be in touch

Great that's all sorted!

Thank you for choosing Brayleys for your service

A member of the team will be in touch shortly to book you in for your appointment, we look forward to welcoming you to the dealership.

Please provide your details below and a member of our team will be in touch

Please provide your details below and a member of our team will be in touch

Fill in your details below and a member of our team will be in touch

Please leave your details and we will call you back as soon as possible to confirm your appointment slot.

Let us know how you would like to receive your virtual appointment in the comments. Eg Zoom, Skype, Whatsapp.

Fill in your details below and a member of our team will be in touch

Fill in your details below and a member of our team will be in touch

By providing your details you consent to us being able to contact you using the methods given above. Read more.